Workers Compensation Insurance

Protect your crew and stay compliant with workers compensation insurance built for food businesses — get a free online quote in 10 minutes.

Workers Comp Designed for the Food Industry

Protection That Stands the Kitchen Heat

Coverage crafted for food trucks, caterers, vendors, mobile food businesses, and restaurants — and the unique risks they face

Simple Compliance With State Requirements

Hassle-free insurance that checks the boxes of your state’s workers compensation requirements

Tailored for How Your Business Hires

Protection for full-time, part-time, temporary, and seasonal employees, as well as uninsured independent contractors

What Is Workers Compensation Insurance?

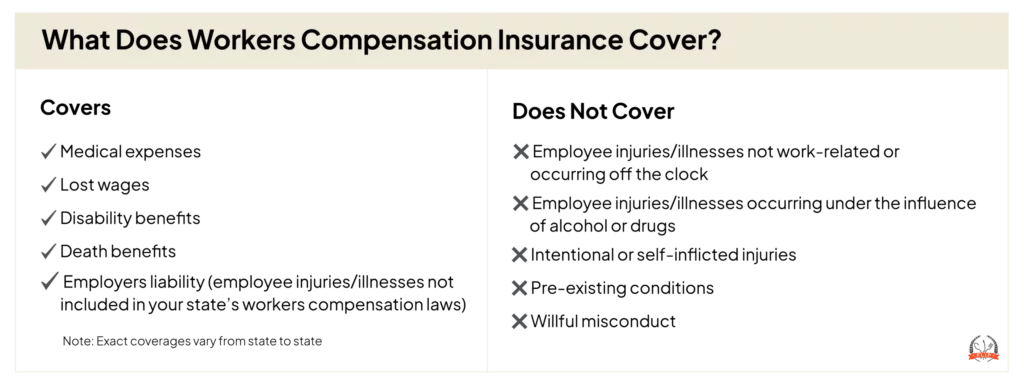

Workers compensation insurance is coverage designed to provide medical benefits and wage replacements to employees who suffer a work-related injury or illness. If someone on your team gets hurt while working for your business, workers comp can help cover their care and time away from work, so the costs don’t come entirely out of your pocket.

Most states require this coverage once you have employees. Texas is the main exception, and rules and exemptions vary by state.

Who Needs Workers Compensation Insurance?

If you run a food or beverage business with full- or part-time employees (or contract workers), you need workers compensation coverage. It’s typically legally required by your state’s Department of Labor if you operate with staff.

Food Liability Insurance Program (FLIP)’s workers compensation is available for businesses like:

Who Is Covered Under FLIP’s Workers Compensation Policy?

FLIP’s policy covers the people who work in small food businesses, including:

- Full-time employees

- Part-time employees

- Temporary or seasonal workers

- Uninsured independent contractors

Every food business hires and operates differently. The general rule: if someone takes orders, cooks food, or otherwise helps keep your business running, you’re responsible if they suffer an injury on the job. Workers comp is built to cover these people: your staff.

A Note on 1099 Workers

Hiring someone as an independent contractor doesn’t automatically remove your exposure if they’re injured while working. In many states, if a contractor doesn’t carry their own workers comp coverage, you, the hiring business, may be held responsible for their medical costs and lost wages. FLIP accounts for situations like these.

How Does Workers Compensation Insurance Work?

FLIP’s workers compensation insurance is made up of two parts that work together: one covers your workers, the other covers you, the business owner.

Part One: Workers Compensation

If an employee is injured or becomes ill because of their job, Part One pays what your state requires for medical treatment, lost wages, and rehabilitation. There are no standard dollar limits on this coverage; it covers what you’re legally obligated to pay under your state’s workers compensation law.

Part One covers:

- Emergency and ongoing medical treatment

- Lost wages during recovery

- Rehabilitation and physical therapy

- Long-term or permanent disability benefits when required

Part Two: Employers’ Liability

Workers comp benefits don’t cover every scenario. If an employee (or their family) sues you directly over a work-related injury or illness, Part Two is designed to step in. This includes situations such as:

- Third-party action-over claims: Your employee is injured by kitchen equipment and sues the manufacturer. The manufacturer turns around and names you in the lawsuit, claiming improper use. Part two can cover your legal defense and any damages.

- Loss of consortium: The spouse of an injured employee sues your business because the injury has affected their relationship or the employee’s ability to provide companionship. Part two can cover these damages.

Unlike Part One, Part Two does have limits.

How Much Does Workers Compensation Cost?

Workers compensation pricing is based on your industry, total payroll, state, and claims history. What you’ll pay depends on your payroll, industry, and state. Most small food businesses find FLIP affordable, with flexible payment options.

The fastest way to find out how much your business will pay is to answer a few questions online and get a personalized quote in about 10 minutes.

What Do Workers Comp Claims Look Like in the Food Industry?

Your workers comp policy can help cover claims like these, so you can focus on the lunch (or dinner) rush and run your business with confidence.

Food Truck Grease Splash

What Happened: While working in a cramped food truck, a line cook sustains a second-degree burn from a grease splash.

How FLIP Protects You: Workers comp steps in to cover your line cook’s medical expenses and a portion of their lost wages during recovery.

A Caterer’s Heavy Lift

What Happened: A seasonal catering assistant injures their lower back after loading a 60-pound chafing dish set into a van for a corporate event.

How FLIP Protects You: Workers comp can cover the medical treatment, physical therapy, and partial wage replacement for your employee. If they later claim the injury was caused by inadequate training and sue, employers’ liability can help pay for your legal defense.

Repetitive Strain at the Bakery

What Happened: A production baker develops carpal tunnel syndrome after rolling dough and packing orders. They require surgery and occupational therapy.

How FLIP Protects You: Part One can cover the surgery and rehabilitation benefits for an employee who becomes ill due to job duties.

What States Is FLIP’s Workers Comp Coverage Available in?

FLIP offers workers compensation insurance in 46 states.

It’s not available in:

- Ohio

- North Dakota

- Washington

- Wyoming

These four states are monopolistic, meaning state law requires employers to purchase workers compensation coverage through a state-run fund rather than a private insurer (like FLIP).

What Information Do I Need to Get a Quote?

We need some details about your business to give you a quote, including your:

- Business type

- Federal Employer Identification Number (FEIN)

- Address

- Phone number

Note: When filling out your application, you must select the business class (e.g., caterer, food truck, etc.) that best describes your business. Selecting the wrong business class can cause delays and lengthen the time it takes for you to get insured.

What Are the Coverage Limits?

Workers Compensation Insurance Coverage

Because workers compensation laws differ from state to state, your coverage limit depends on your state’s specific statutory requirements.

Employers’ Liability Coverage Limits

The maximum coverage for damages resulting from bodily injury by disease for any number of employees.

$1,000,000 Policy Limit

The maximum coverage for bodily injury to one or more employees in any one accident.

$1,000,000 Each Incident

The maximum coverage for damages resulting from bodily injury by disease for any number of employees.

$1,000,000 Each Employee

Why FLIP for the Best Workers Compensation Insurance?

Quick Application Process

Get a workers compensation insurance quote in about 10 minutes — roughly the time it takes to bake a dozen chocolate chip cookies.

100% Online Quote

Most companies make you speak with an agent to get a quote. With FLIP, get your free quote simply by filling out our online application.

Flexible Payment Options

FLIP makes it easy for you to pay your way. Choose between annual, quarterly, semiannual, and monthly* plans.

*Monthly payments are only available for policies exceeding $1,000 per year.

Food & Beverage Businesses Love FLIP

See why FLIP is a trusted name in the food industry — these reviews say it all.

Yes. Part Two of FLIP’s workers compensation policy can protect you if your injured employee sues a third party for a work-related injury or illness that isn’t included in your state’s benefits, if that third party attempts to hold you responsible.

Yes. If the spouse of your injured employee sues you because that employee is no longer able to give them the companionship, support, or services they were able to before their injury or death, Part Two of your policy can cover those damages.

All states except Texas require employers to purchase this coverage. However, exact requirements and exemptions differ between states, so check workers’ compensation laws in your state to confirm what coverage you need.

Yes, FLIP’s policy covers full-time, part-time, and temporary employees. If someone is on your payroll — regardless of how many hours they work — they’re covered.

It depends on whether they carry their own workers comp coverage. If a contractor you hire doesn’t have their own policy, FLIP’s workers’ compensation can cover them as an uninsured independent contractor.

This is one of the most common gaps in small food business coverage and a major source of unexpected liability.

No, FLIP’s policy does not cover volunteers, including unpaid friends or family members who are helping your business. Ensure your hiring relationships are laid out with clear contracts to keep your business (and those working for it) safe.

Your workers compensation policy covers both! Part One is designed to cover medical costs, lost wages, and rehab for injured employees. Part Two (employers’ liability) can cover your legal defense and damages if an employee sues you over a work-related injury or illness.

If your food truck operates with hired staff, yes, you need workers compensation to stay compliant with state labor laws and to protect your workers in case they get injured on the job.