Restaurant Insurance Cost

Exactly how much does restaurant insurance cost, and how is your premium determined? We have answers to those questions and more with this comprehensive cost breakdown.

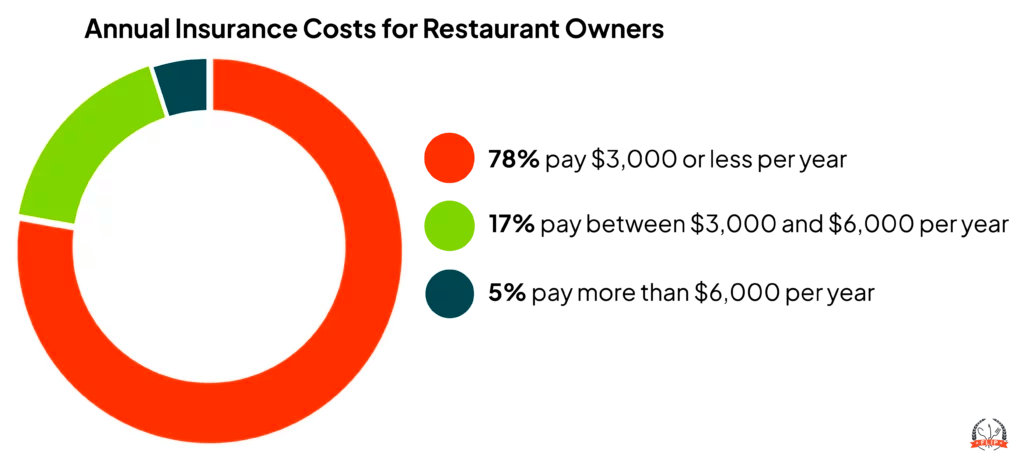

How Much Does Restaurant Insurance Cost?

The average restaurant insurance policy costs $2,500 a year, or $208.33 a month, with most policyholders paying between $800 and $11,000 annually.

Your premium can vary depending on which additional coverages you select and your business’ gross annual income.

What Factors Affect Restaurant Insurance Cost?

There are several factors that impact the cost of your restaurant insurance premium, including:

- Your gross annual income: Restaurants that make more per year have higher premiums than those that make less

- The type of restaurant you own: Full-service restaurants typically cost more to insure than carryout locations

- Your restaurant’s location: Premiums tend to be higher for restaurants in areas with higher population density and/or more crime

- Your payroll: More employees equal higher premiums

- Your claims history: If you have a history of filing claims, your business poses more of a risk to your insurance company, so your premium may be higher

- Whether you rent or own your location: If you own your building, you need additional coverage to insure it (commercial property insurance)

- Whether you serve alcohol: Restaurants that serve alcohol are exposed to more risks and require additional coverage (liquor liability insurance)

Can I Reduce My Restaurant Liability Insurance Cost?

The best way to reduce the cost of your coverage is to incorporate risk management strategies into your daily restaurant operations. Taking preventative measures decreases your risk of an accident happening, which means you’re less likely to need to file a claim and have your premium go up.

Here are a few risk mitigation strategies all restaurant owners should follow:

- Prevent slips, trips, and falls with non-slip mats, wet floor signage, and by promptly cleaning up any spills

- Stay on top of equipment maintenance by having all equipment serviced per the manufacturer’s recommendations

- Reduce fire hazards by regularly cleaning exhaust hoods/ducts, keeping flammable materials away from heat and flame, and training your staff on proper fire procedures

- Strengthen your food safety protocol with FIFO (first in, first out) inventory rotation, creating temperature logs for refrigerated goods, and using color-coded cutting boards to avoid cross-contamination

- Decrease the chances of employee injuries by conducting mandatory safe-lifting training, regular monitoring, and an established accident-reporting procedure

- Prevent alcohol-related accidents (if applicable) by checking all IDs, cutting off service for overly intoxicated patrons, and ensuring servers are up-to-date on alcohol safety training

Why FLIP for the Best Restaurant Insurance?

Top-Rated Coverage

Customizable Policies

Affordable Pricing

Fast, Online Quote

Trusted by 40,000+ Businesses

15+ Years Experience

Coverage Details & Limits

General Liability Aggregate Limit

Starts at $2,000,000

Products-Completed Operations Aggregate Limit

Starts at $2,000,000

Personal and Advertising Injury Limit

Starts at $1,000,000

General Each Occurrence Limit

Starts at $1,000,000

Damage to Premises Rented to You Limit

Starts at $50,000

Liquor Liability Occurrence & Aggregate Limit

Starts at $1,000,000

How Do I Get a Quote?

1. Start your online application

2. Fill out the required information about your business (name, FEIN, payroll, etc.)

3. Submit your application, and a licensed agent will contact you with your quote!

FAQs About the Cost of Restaurant Insurance

Which Coverages Do Restaurants Need?

Restaurants typically need the following types of coverage:

- Business income interruption: Can cover lost income and operating expenses if you close your restaurant due to a covered incident (e.g., fire)

- Commercial property: If you own your building, this covers damage to it and its contents (e.g., furniture, equipment, etc.)

- Cyber liability: Designed to cover expenses stemming from data breaches or other cyberattacks

- Damage to premises rented: If you rent your building, this covers damage to it within the first seven days of renting, then only fire damage afterwards

- Employment practices liability (EPLI): Covers costs stemming from employee claims of harassment, discrimination, or wrongful termination

- Equipment breakdown: Can cover the cost of repairing or replacing your kitchen equipment if it fails

- General liability: Covers expenses stemming from injuries to others or damage to their property caused by your restaurant operations

- Liquor liability: If you serve or sell alcoholic beverages, this covers legal expenses if an intoxicated guest causes injury or property damage to others

- Product liability: Designed to cover your expenses if a customer gets sick or injured from something you served them

- Workers compensation: Covers your state’s mandatory workers compensation benefits if your employee suffers a work-related injury or illness (e.g., lost wages, medical bills, rehabilitation, etc.)

Why Does Liquor Liability Change My Premium So Much?

Serving alcohol comes with a lot of risk for your business. If an intoxicated guest causes a car accident after drinking at your restaurant, your state’s dram shop laws could hold you legally responsible for the injuries or property damage they cause.

Liquor liability claims can be extremely expensive, sometimes costing hundreds of thousands — or even millions — of dollars. Insurance premiums are higher for liquor liability coverage to offset the increased risk.

Do Landlords Accept FLIP’s Proof of Insurance?

Yes, FLIP’s coverage satisfies most landlord requirements. If your landlord requires you to carry coverage with specific limits, please let your customer service representative know after you submit your application so they can assist you.

Can a Restaurant Operate Without Insurance?

Technically, yes, but it’s often illegal or impossible to get the licenses you need to run your restaurant without a Certificate of Insurance (COI). If you’re caught operating your restaurant without the proper coverage, you could face fines, have your licenses revoked, or be forced to close.

Being uninsured also means that if an accident happens, you may have to pay out-of-pocket for any resulting expenses. With insurance, some — or all — of those costs can be covered by your policy.

What Coverage Limits Should a Restaurant Carry?

The limits you need can vary depending on the size of your restaurant and your revenue, but here are some typical limits you may be expected to meet:

- General liability: $1,000,000 per occurrence / $2,000,000 aggregate

- Liquor liability: $1,000,000 per occurrence / $2,000,000 aggregate

- Commercial property: Replacement cost

- Business interruption: Equal to 6–12 months’ revenue

- Equipment breakdown: $50,000 per occurrence / $100,000 aggregate

Why Is Restaurant Insurance So Expensive?

Restaurants face multiple types of high-severity risks, and insurance companies price policies based on the likelihood and cost of claims. Since restaurant claims can be expensive, coverage tends to cost thousands of dollars a year.

However expensive your premium may be, the cost of a typical claim is often much higher. Think of insurance as an investment in your restaurant’s financial safety. By paying a premium every year, you gain coverage for claims that might otherwise bankrupt your business or put you under serious financial stress.

If I Lease My Commercial Kitchen to Renters, Do I Need Restaurant Insurance?

If you own a commissary or rent space to other food business owners, you need commercial kitchen insurance. We offer this coverage through our sister company, Insurance Canopy. Fill out an online application today and protect your kitchen from the expense of property and liability claims!

Reviewed by: Kyle Jude

Kyle Jude is the Program Manager for Food Liability Insurance Program (FLIP). As a dedicated program manager with 10+ years of experience in the insurance industry, Kyle offers insight into different coverages for food and beverage business professionals who are looking to navigate business liability insurance.